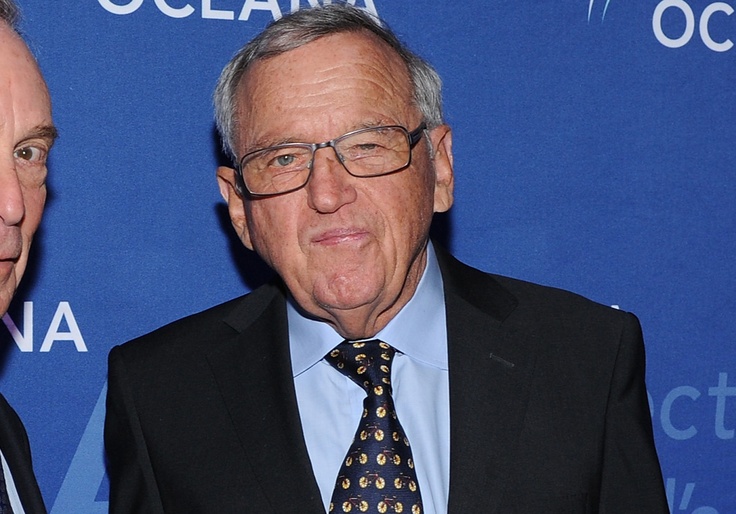

Alan Greenspan, Fed Chair Through Prosperity and Crisis, Dies at 100

Alan Greenspan, who in nearly two decades as chair of the Federal Reserve nurtured a long run of prosperity, navigated crises and was a powerful and polarizing force in shaping market-friendly policies, died on Monday at his home in Washington. He was 100.

The cause was complications of Parkinson’s disease, his wife, Andrea Mitchell, the chief Washington correspondent and chief foreign affairs correspondent for NBC News, said in a statement.

The preeminent economic policymaker of his time and arguably the most recognizable economist of any era, Greenspan led the central bank under four presidents of both parties from 1987 to 2006.

Much of his tenure coincided with a streak of affluence in which he stood as the embodiment of a triumphant, post-Cold War strain of American capitalism: optimistic, faithful in the power of markets to improve living standards, captivated by the power of technology and averse to regulation.

But the ideological stamp he put on policymaking came to be associated as well with the destructive consequences of forces that emerged on his watch, including deregulation of banking and Wall Street, the loss of American jobs to free trade and persistent concerns about bubbles in stock and housing prices.

Even as Greenspan skillfully managed interest rates in a way that kept the economy humming along, he remained leery of confronting a danger he well recognized: that the low-inflation, easy-money environment he had helped create was putting the United States at risk by fueling unsustainable investment booms. And he remained reluctant to act as banks and investment firms adopted complex new trading techniques that would come to wreak great damage.

At the Fed, he was remarkably successful at what he considered the central banker’s primary task of holding down inflation. He also helped the United States deal with periodic shocks, including a stock market crash just weeks after he took office, the near-meltdown of Asian financial markets a decade later and the aftereffects of the Sept. 11, 2001, terrorist attacks.

Only after he stepped down in early 2006 — and especially following the crisis on Wall Street in 2008, the near-collapse of the mortgage market and the ensuing deep recession — were his legacy and philosophy challenged in a concerted way.

By that point, one group of critics blamed him for not heading off a housing bubble by pushing interest rates higher. Another accused him of promoting a corrosive free-market fundamentalism that left the financial system to operate unchecked as it adopted increasingly risky practices.

After overseeing a period of immense wealth creation, he was often portrayed as among those responsible for the 2008 crisis and the economic and political shocks that followed it.

His failure to put greater focus on keeping the financial system stable once he had shown he could keep inflation in check “was Greenspan’s most consequential error, one that he did not have to make,” his biographer, Sebastian Mallaby, concluded.

His record — and the degree to which he deserves either the praise or the blame heaped on him — remains a subject of intense debate. There is no doubt that he was a pivotal figure during a period of immense ferment in the economy and deep ideological divides over how to manage it.

At the peak of his fame, as the economy boomed in the late 1990s, his merest phrase could send the markets sharply up or down, and his face, behind thick glasses, was as familiar as any movie star’s.

In public, he often spoke in an elliptical jargon that even his fellow economists had trouble deciphering.

Behind the scenes in Washington, Greenspan was a master of the political power game. Schooled by his experiences as a policy adviser to Richard Nixon’s 1968 presidential campaign and his role as President Gerald Ford’s chief economist, he developed into a wily operator who skillfully protected the Fed’s independence while shaping the agendas of successive presidents and steering legislation on Capitol Hill.

His predecessor, Paul A. Volcker, had established that the central bank could hold off political pressure for lower interest rates with a tight-money strategy in the late 1970s and early 1980s. In the process, Volcker gave the Fed tremendous credibility in the financial markets and bequeathed to Greenspan plenty of room to shape policy in Washington.

Greenspan used his influence shrewdly on issues that, strictly speaking, went beyond his mandate at the Fed, weighing in regularly to shape policy on taxes, the budget deficit and trade. A Republican with strong libertarian leanings — in his younger days he was an acolyte of Ayn Rand, and he was appointed to the Fed by President Ronald Reagan — he nonetheless managed to infuriate Republicans as well as Democrats even as he won reappointment from presidents of both parties.

Allies of President George H.W. Bush blamed Greenspan in part for Bush’s loss of the White House to Bill Clinton in 1992, saying Greenspan had kept interest rates too high as the economy was coming out of recession. Greenspan built close ties to Clinton and his team, helping to infuse the Democratic administration with a distinctly market-friendly stance on financial regulation and encouraging Clinton early on to embrace deficit reduction, over the objections of liberals.

But in 2001, when Greenspan backed President George W. Bush’s big income-tax-cut package, Democrats howled that he had sold out his deficit-reduction beliefs to curry favor with the new Republican administration.

The Washington Life

Alan Greenspan worked all the angles, cultivating allies across the aisle and at both ends of Pennsylvania Avenue. Ever-present in social Washington, he was a genial if reserved figure as he mingled at parties with Supreme Court justices, cabinet secretaries and journalists, sporting an amused smile and offering a soft handshake.

He dated Barbara Walters of ABC News in the late 1970s. (“I’m not threatened by a powerful woman,” he wrote in his autobiography.) In 1997, he married Mitchell, who by his account never entirely forgave him for discussing antitrust policy on their first date many years earlier; their wedding was presided over by Justice Ruth Bader Ginsburg. Mitchell is Greenspan’s only immediate survivor.

He was an avid tennis player, picking the game up in earnest on the White House court while serving in the Ford administration and pursuing it in spirited competition well into his 80s against a succession of Treasury secretaries and senior officials from both parties.

He eschewed formulas and rules other central bankers often relied upon in favor of a more intuitive approach based on deep analysis of data about decisions being made by businesses, consumers and investors. (He admitted to doing some of his best thinking while soaking in a hot bath.)

At the Fed, he perceived how a set of powerful forces, chief among them rapid advances in technology and increased global competition, were altering the outlook for inflation and therefore the economy’s ability to grow and create jobs without undue upward pressure on prices.

Because of technology, Greenspan concluded in the mid-1990s, all kinds of industries were able to produce more for less. In economic terms, they were generating improved productivity gains.

Acting on that belief, Greenspan tended to keep interest rates lower than traditional economic models suggested they needed to be. As a result, he was able to allow the economy to keep expanding at a rapid clip even as unemployment descended to levels that previous generations of central bankers would have regarded as warning signals of inflation and a reason to raise rates.

For much of his time as Fed chair, especially in the late 1990s, Greenspan appeared to be right. His policies helped create conditions in which price increases were negligible, the economy created millions of new jobs, businesses were able to borrow at attractive rates and the stock market boomed.

But the productivity gains began fading away after the turn of the century. And even as monetary policy under Greenspan appeared to have triumphed to a remarkable degree over the business cycle, he and the Fed were confronted with what proved to be troublesome and ultimately disruptive forces that they failed to fully understand, much less tame.

The Revenge of Risk

The cheap-money environment in the United States coincided with two other developments. The first was a sense among investors that the Greenspan Fed would always step in to curb the damage from financial crises, limiting their risk and arguably breeding complacency.

The other was the emergence of a vast pool of global savings, generated in large part by rapid growth in China and other developing nations. That capital washed over borders in search of profitable investment opportunities, often driving down long-term interest rates, like those on mortgages. But it could be fickle, fleeing again when trouble arose or opportunity beckoned elsewhere.

As it helped fuel first the stock market and then the housing market in the United States, the global savings pool made many households wealthier than they had ever been, at least on paper. It also helped push asset prices to what proved to be unsustainable levels in the United States and elsewhere, creating boom and bust cycles.

Greenspan had long been interested in the interplay between the economy and prices of assets — stocks, bonds and homes. He set off financial tremors in 1996 simply by raising the question publicly of whether “irrational exuberance” was creating bubbles.

He proved reluctant to intervene to head off or prick bubbles when they appeared during his time in office, even as he fretted about the problem in private. Greenspan often suggested in public that it was all but impossible to avert or deflate bubbles without damaging the economy — in part, he said, because it is hard to identify a bubble until it has burst.

“It is far from obvious that bubbles, even if identified early,” Greenspan said in 2004, “can be preempted at lower cost than a substantial economic contraction and possible financial destabilization — the very outcomes we would be seeking to avoid.”

Greenspan’s general philosophy, and his influence, survived the bursting of the technology-stock bubble in 2000, which foreshadowed the end of what at the time was the longest economic expansion on record — 10 years, from 1991 to 2001.

The economy bounced back within a year, despite the financial and psychological shock of the Sept. 11 attacks. Greenspan turned aside warnings that the real estate market was becoming a bubble during the first decade of the new century and continued to keep interest rates at relatively low levels.

By the time the mortgage market started to implode in 2007, triggering the broader crisis that led to the worst recession since the 1930s, Greenspan had left office. He faced intense criticism that he had failed in his role as a financial regulator and that his easy monetary policy had backfired, destroying much of the wealth that it had helped to create.

One of the most stinging critiques came from John B. Taylor of Stanford University, one of the foremost monetary economists and the developer of a widely accepted approach to determining the proper level of official interest rates. Writing in The Wall Street Journal in early 2009, Taylor laid the blame for the housing bubble squarely, if not solely, on the Greenspan Fed, saying it had kept rates too low for too long.

“The Fed held its target interest rate, especially in 2003-05, well below known monetary guidelines that say what good policy should be based on historical experience,” Taylor wrote. “Keeping interest rates on the track that worked well in the past two decades, rather than keeping rates so low, would have prevented the boom and bust.”

In the face of that kind of criticism, Greenspan spent much of his time after leaving office in February 2006 defending his legacy. Known at the height of his power by terms like “maestro” and “oracle,” he confessed in late 2008 to being “in a state of shocked disbelief” at the failure of market forces to avert the economic calamity. His belief that markets were guided by rational actors, he acknowledged, had been shaken.

More even than his conduct of interest rate policy, his laissez-faire approach to the regulation of increasingly complex and interconnected financial markets exposed him to second-guessing.

Derivatives and the Markets

The criticism was focused in particular on his attitude toward derivatives. Financial instruments that allow companies and investors to spread risk, derivatives were later blamed for spreading and accelerating the financial shocks that rocked the economy in 2007 and 2008.

Greenspan played a key role in the late 1990s in heading off efforts to regulate derivatives more tightly. He was close allies in those years with most members of the Clinton economic team, including Treasury Secretary Robert E. Rubin and Larry Summers, Rubin’s deputy and successor. (The three were dubbed “The Committee to Save the World” on a Time magazine cover in 1999 after addressing a succession of financial crises.)

Together with them, Greenspan worked to block a proposal put forward in 1998 by Brooksley E. Born, the head of the Commodity Futures Trading Commission, that called for greater transparency in derivatives trading and more cushions against losses.

Greenspan and his allies asserted that the proposed regulation could destabilize the markets. Throughout the debate, Greenspan argued that the financial markets, and investment firms themselves, would do a better job of policing excess risk than the government could ever do.

From Juilliard to Ayn Rand

Alan Greenspan was born on March 6, 1926, in New York City. He was the only child of Herbert and Rose (Goldsmith) Greenspan. His parents divorced when he was 5, and he was raised by his mother in the Washington Heights section of Manhattan.

With the enthusiastic encouragement of his mother, who enjoyed singing, dancing and playing the piano, he became an accomplished musician in his teenage years. After graduating from George Washington High School, he went on to the Juilliard School and spent several years playing saxophone in a swing band.

During the band’s gigs, Greenspan would spend breaks reading books he had borrowed from the library. “And one day I got a book out on business, finance or something on the stock market,” he said in a 1989 interview with The New York Times Magazine, “and I found it really fascinating.”

Recognizing that economics might prove a more fruitful field for him than music, Greenspan left Juilliard and entered New York University, where he earned a bachelor’s degree in 1948 and a master’s in 1950, both in economics. He started work on his doctorate at Columbia University, where he studied under Arthur Burns, who would later become Fed chair. Greenspan eventually received a doctorate from NYU in 1977.

Greenspan was married in 1952 to Joan Mitchell (later Joan Mitchell Blumenthal), a painter and writer; the marriage ended after a year.

His specialty was forecasting, built around intense study of arcane statistics rather than grand theories. As he was building a professional reputation during the 1950s, Greenspan was also developing an intense free-market philosophy, one that was heavily influenced by Ayn Rand, whose novels espoused laissez-faire capitalism built around a “rational selfishness,” or the idea that society functions best when individuals pursue their self-interest.

Through his first wife, Greenspan met Rand in 1952 and soon became part of her inner circle, spending hours debating the relationships among individuals, governments and markets. Greenspan, who had come of age during the reign of Keynesian theory — which came to justify the idea of an activist government role in the economy, including the use of government spending to stimulate growth and redistribute wealth quickly — found his assumptions under sustained intellectual attack from Rand.

Eventually, Greenspan said, Rand taught him that capitalism was not only efficient and practical, but moral.

In the GOP Camp

Greenspan first got involved in politics in 1967, when he signed on as an adviser to Nixon’s presidential campaign, an experience that exposed him to the trade-offs between ideological principle and winning campaigns. In 1974, shortly before Nixon resigned in the Watergate scandal, Greenspan was named chair of the White House Council of Economic Advisers, a post he took up just after Ford took office, a period when the nation was enduring not just the political shock of Watergate but also the economic shock of soaring oil prices and roaring inflation.

After Ford’s loss to Jimmy Carter in 1976, Greenspan remained active in Republican politics. At the 1980 Republican convention, he played a key role in negotiating an ultimately aborted deal that would have made Ford the vice-presidential nominee on the Republican ticket with Reagan as part of a power-sharing arrangement.

After Reagan’s election as president, Greenspan was handed the sensitive job of heading a commission to keep the Social Security system from running out of money. In 1983, the commission recommended a mix of benefit cuts and tax increases. Given the real danger that Social Security would soon be unable to meet its obligations, most of the recommendations were adopted by Congress, and Greenspan’s stock in Washington went up.

Over the next few years, Greenspan was a regular presence in Washington, advising the Reagan administration, testifying before Congress and serving on various commissions.

As early as 1986, there was speculation in Washington and on Wall Street that Greenspan would succeed Volcker as Federal Reserve chair should Volcker not be nominated for a third four-year term in 1987. When Volcker, whose rigorous anti-inflation strategy brought on two recessions but largely succeeded in breaking a pattern of spiraling prices, decided to step down, the Reagan administration viewed Greenspan as the obvious choice.

On Aug. 3, 1987, Greenspan’s nomination was approved by the Senate on a 91-2 vote, and eight days later he was sworn in as the Federal Reserve’s 13th chair.

The Crash of ’87

Greenspan took office very much in Volcker’s shadow, and with many people both on Wall Street and in Washington wondering if he was up to the job. His first test came quickly, when the stock market crashed on Monday, Oct. 19, 1987, falling 508 points, or 22.6%, a bigger drop even than on Black Friday in 1929.

The question until that point had been whether Greenspan would show the same inflation-fighting fortitude Volcker had shown — and especially whether he would be able to resist pressure from a Republican White House to keep the economy humming along through the 1988 election.

The market crash forced Greenspan to shift, at least temporarily, from tightening monetary policy to an abrupt easing. He flooded the financial system with money, greasing the system and averting brokerage and bank collapses. The economy ended up suffering no lasting harm.

The episode brought Greenspan new respect. Over the next few years, he gradually developed the same kind of clout within the Fed that Volcker had enjoyed at the peak of his power in the early 1980s, with other Fed governors and the presidents of the Federal Reserve Banks reluctant to challenge his authority or question his judgment.

By the late 1990s, Greenspan had achieved what most economists considered price stability — Consumer Price Index increases below 2%, and a psychological change among businesses and consumers, who no longer factored inflationary expectations into their planning and who benefited from the ensuing drop in long-term interest rates.

With inflation largely under control, Greenspan, starting in the mid-1990s, increasingly confronted challenges stemming from an ever-more-complex global financial system.

Abroad, there were crises in Mexico, the emerging Asian economies and Russia that at various points threatened not only investors and financial institutions but the livelihoods of working Americans who found their jobs and savings tangled up in policy decisions made in far-off capitals and boardrooms.

Within the Fed, there were debates about deflation, a chronic decline in prices and wages that appeared to have beset once-mighty Japan.

With the economy at home booming, Greenspan chose to sidestep concerns about the dangers of an increasingly complex financial system and the risks that stock and later housing prices might collapse and bring the economy down with them.

The bursting of a housing bubble, Greenspan said in 2003 as concerns grew about just such an outcome, was “most unlikely.”

On Jan. 31, 2006, at 79, Greenspan engineered a small rise in interest rates at a Fed policy-setting session, his last act in office. A few hours later, the Senate confirmed his successor, Ben Bernanke. Greenspan departed with a souvenir — his chair from the central bank’s vast boardroom — and what seemed at the time to be the likelihood of a secure legacy.

—

This article originally appeared in The New York Times.

By Richard W. Stevenson/Doug Mills

c. 2026 The New York Times Company

The post Alan Greenspan, Fed Chair Through Prosperity and Crisis, Dies at 100 appeared first on GV Wire.

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Comments (0)